KYC for eVisa Payments: What Travel Brands Need to Know

Selling eVisas and other digital travel authorizations inside the booking flow is quickly becoming a high-performing ancillary. But the moment you take payment for an eVisa, you are also stepping into a tighter compliance zone: card-network rules, payment service provider (PSP) requirements, sanctions screening expectations, anti-fraud controls, and, in some cases, formal AML and KYC obligations.

This guide explains KYC for eVisa payments in practical terms for airlines, OTAs, cruise lines, tour operators, and TMCs: what “KYC” really means in this context, when it applies, which operating model changes your responsibilities, and how to implement controls without hurting conversion.

Note: This article is educational, not legal advice. Requirements vary by jurisdiction, product structure, and who is the merchant of record. Always confirm your obligations with your legal and compliance teams.

KYC for eVisa payments: what it actually means (and what it doesn’t)

In travel, “KYC” gets used loosely. For payments, it has a specific compliance meaning.

KYC (Know Your Customer) is the process of verifying a customer’s identity to help prevent fraud, money laundering, and sanctions evasion.

KYB (Know Your Business) is the same concept applied to business customers (for example, agencies, affiliates, or sub-distributors).

AML (Anti-Money Laundering) is the broader program (policies, monitoring, reporting) that often includes KYC/KYB.

Sanctions screening is checking whether individuals or entities are on restricted lists or are located in sanctioned jurisdictions (for example, U.S. OFAC or the EU’s sanctions regimes).

What KYC is not: it is not the same as the traveler’s immigration eligibility checks. A traveler can be a legitimate person and still fail visa requirements, or be eligible for a visa but represent a payment or fraud risk.

Why travel brands are paying more attention now

Even if you do not consider yourself a “financial institution,” eVisa payments can trigger enhanced scrutiny because they are:

- Cross-border by nature (international travelers, international destinations, multi-currency).

- Digitally delivered (no physical shipping proof, which changes dispute dynamics).

- Time-sensitive (last-minute purchases and urgent processing are statistically higher risk).

- High-consequence (a failure can lead to denied boarding, refunds, chargebacks, and reputational damage).

On top of that, regulators and banks increasingly expect risk-based controls aligned to global standards such as the FATF recommendations. In practice, your PSP, acquirer, and card networks may be the first to enforce “KYC-like” requirements through underwriting, monitoring, or account reviews.

The #1 determinant of your KYC obligations: your payment operating model

For most travel brands, the question is not “Should we do KYC?” but “Who is responsible for KYC, and at what level?” That depends on your role in the money flow.

Common models for eVisa payments

| Model | What the traveler sees | Who typically takes the payment | Who typically handles KYC/KYB with the PSP/acquirer | Practical implication for travel brands |

|---|---|---|---|---|

| Travel brand is Merchant of Record (MoR) | eVisa sold by airline/OTA | Travel brand | Travel brand | Highest control and highest responsibility. Expect stronger underwriting, monitoring, and dispute management obligations. |

| eVisa provider is MoR | eVisa sold “powered by” partner | eVisa provider | eVisa provider | Travel brand reduces payments compliance scope, but still needs good disclosure, customer support alignment, and fraud handoffs. |

| Referral / outbound checkout | Traveler is redirected | eVisa provider or government portal | eVisa provider / portal | Lowest payments responsibility, but typically lower attach rate and weaker end-to-end experience. |

| Split flows (fees + service) | Mixed checkout experience | Varies | Varies | Complexity increases. Refund logic, chargebacks, and disclosures must be very clear. |

The model you choose affects not only KYC duties, but also your ability to optimize ancillary revenue and user experience. If you are evaluating integration patterns, SimpleVisa has a good primer on delivery options in API vs. White-Label App: Which Visa Integration Model Suits You?.

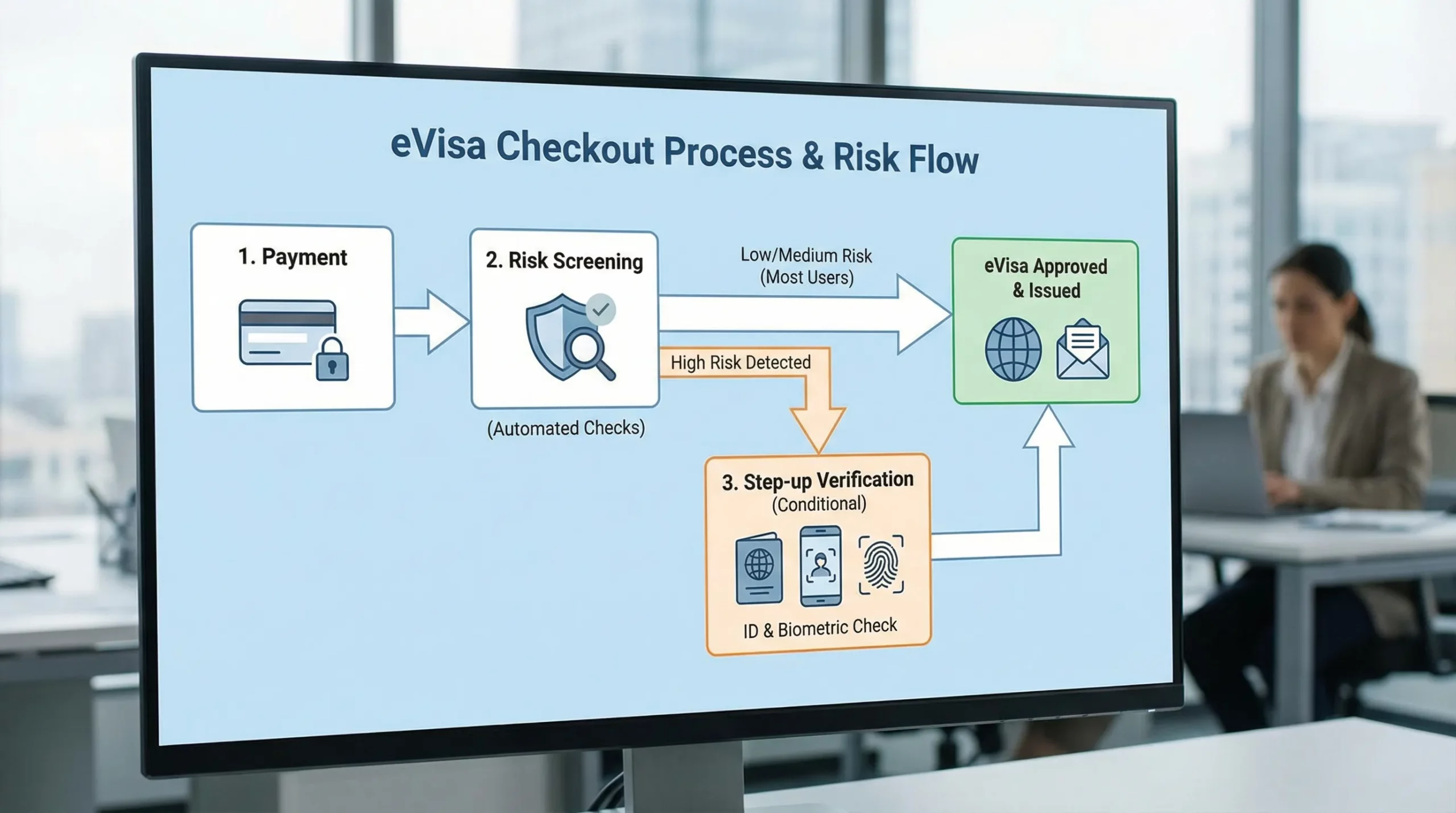

What “good” KYC looks like for eVisa payments (risk-based, not one-size-fits-all)

In most card-based e-commerce flows, you usually do not need to collect passport-style identity documents for every traveler just to accept a payment. However, you do need a risk-based framework that answers:

- Who is paying, and can we link them to a real person?

- Does the transaction show money-laundering or sanctions indicators?

- Can we defend disputes with a clean audit trail?

Baseline data typically used (low friction)

For most travel brands, baseline controls focus on:

- Card and payment authentication signals (for example, 3DS/SCA results where applicable)

- Billing name and address (AVS where supported)

- Email, phone, and IP address

- Device and behavior signals (velocity, geolocation mismatch, abnormal patterns)

- Clear order descriptors and receipts

Step-up verification triggers (when to ask for more)

Instead of forcing document checks on everyone, many brands use step-up verification only when risk is elevated.

Common step-up triggers in eVisa contexts include:

- Payer and traveler mismatch (especially for single-traveler bookings)

- High transaction velocity (many applications in a short window)

- Repeated failed payments followed by success (possible card testing)

- IP geolocation inconsistent with billing country and travel origin

- Elevated dispute rate from a specific channel, affiliate, or market

- Unusual refund behavior (rapid refund requests, partial refunds, “change of passenger” attempts)

Step-up actions can include:

- Stronger 3DS challenge routing

- Email/phone verification

- Manual review for edge cases

- Document verification for the payer (only when necessary)

Sanctions and restricted geography: the often-missed part

Because eVisa payments are inherently international, sanctions risk becomes operationally relevant faster than many travel teams expect.

Travel brands should align with their compliance teams on:

- Which sanction regimes apply (commonly U.S. OFAC, EU, UK)

- How screening is performed (PSP tooling, internal controls, or vendor processes)

- What happens when a booking involves a restricted jurisdiction

A practical starting point is understanding your exposure under OFAC sanctions programs if you do business with U.S. payment rails, U.S. entities, or U.S. customers.

UX reality: KYC controls can kill conversion if implemented poorly

If you sell eVisas as an ancillary, you are optimizing a funnel. The goal is to control risk without introducing avoidable friction.

Patterns that tend to work well in travel checkouts

Progressive disclosure: Ask only what you need now. Collect additional data only if the traveler proceeds or if risk signals require it.

“Frictionless by default” authentication: Use modern 3DS strategies where the experience remains seamless for low-risk customers, and challenges appear only for higher-risk transactions.

Clear copy at the point of friction: If you must ask for extra verification, explain why in plain language (security, fraud prevention, traveler protection) and set expectations for how long it takes.

Minimize re-entry: Autofill and validation reduce errors. (Form friction is a top abandonment driver in visa flows, as discussed in Why Travelers Abandon Visa Forms, and 6 UX Fixes That Convert.)

What your ops team needs on day one (not after the first dispute)

KYC is not only a product or payments topic. It touches customer support, finance, fraud, and legal.

Chargebacks: assume they will happen

Because eVisas are digital, disputes can be harder to win without a tight record of:

- What the customer agreed to (terms, delivery expectations, refund policy)

- What was delivered (status updates, confirmation, timestamps)

- Who initiated the transaction (device, IP, authentication result)

If your visa program is still manual-heavy, you may also be losing money in hidden operational costs. See The Hidden Costs of Manual Visa Processing (and How to Eliminate Them).

Refunds: where fraud and AML risks often show up

Refund logic is a common weak spot. Consider controls for:

- Refunds to the original payment method only

- Limits on partial refunds unless a policy condition is met

- Review triggers for repeated refund requests across identities/devices

- Clean separation between government fees and service fees (where applicable)

Data retention and privacy: collect less, protect more

KYC and fraud tooling can quickly lead to “data sprawl.” Ensure you have:

- Data minimization rules (collect only what you need)

- Retention schedules aligned with legal, tax, and dispute timelines

- Access controls and audit logs

- Vendor DPAs and security reviews

On card security specifically, your team should align with PCI expectations. The official reference point is the PCI Security Standards Council.

A practical KYC readiness checklist for travel brands selling eVisas

Use this as an internal alignment tool across Product, Payments, Risk, Legal, and CX.

Commercial and product decisions

- Who is the Merchant of Record for the eVisa transaction?

- Are you bundling eVisa fees with travel, or selling as a separate line item?

- Do you support high-risk corridors or last-minute “express” options?

Compliance and controls

- Which sanctions regimes apply to your business and payment rails?

- What identity checks does your PSP enforce, and what is your escalation path?

- What step-up verification triggers will you use (and who reviews them)?

Operational preparedness

- Are your refund rules explicit and easy for support to apply consistently?

- Do you have dispute evidence templates (receipts, delivery proof, logs)?

- Can you trace each transaction end-to-end in an audit trail?

Where a visa management platform fits (and what to ask vendors)

If you are embedding an eVisa flow, your vendor choice impacts both conversion and risk posture.

When evaluating solutions, ask about:

- Payment model options (MoR vs referral vs embedded)

- How the system logs events (submission, payment, approvals, refunds)

- Data handling (minimization, retention, encryption)

- Controls that support your fraud and dispute processes

For a broader view of how automated document workflows reduce operational and compliance risk, see What Is Travel Document Automation? Definitions, Benefits, and Myths.

Frequently Asked Questions

Do travel brands need full KYC for every eVisa purchase? Not always. Many card-based e-commerce flows rely on PSP underwriting plus risk-based fraud controls, with step-up verification only for high-risk transactions.

What’s the difference between KYC and KYB in an eVisa program? KYC verifies individuals (travelers or payers). KYB verifies businesses (for example, agencies or resellers) and is most relevant when you onboard partners who generate transactions.

If our eVisa partner is the merchant of record, are we “off the hook”? Your payments compliance burden is usually lower, but you still need strong disclosures, customer support alignment, and processes for fraud handoffs and traveler complaints.

How does sanctions screening relate to eVisa payments? Cross-border travel creates exposure to restricted jurisdictions and sanctioned persons risk. Depending on your payment rails and markets, screening expectations can come from regulators, banks, or card-network programs.

What’s the biggest operational risk if we ignore KYC-related controls? Disputes and chargebacks are the fast-moving risk, followed by PSP account reviews, reserve requirements, or termination if your dispute rate or fraud patterns exceed thresholds.

Build an eVisa checkout that converts, without compliance surprises

If you are adding eVisas as an ancillary, the best time to design KYC, sanctions, and dispute controls is before you scale volume.

SimpleVisa helps travel brands streamline the visa application journey through embedded integrations, a white-label app, or data services, so you can offer guided eVisa applications and grow ancillary revenue.

Explore integration options at SimpleVisa or start with the technical overview in How eVisa APIs work: Step by Step, then book a demo to discuss the right operating model for your payments and compliance setup.