Visa Chargebacks: Root Causes and Prevention Checklist

Chargebacks are painful in any industry, but visa and travel authorization sales add a unique layer of complexity: split fee components (government vs service), time-delayed fulfillment, strict traveler eligibility rules, and high customer anxiety right before departure.

For travel brands, visa chargebacks are more than a payment issue. They can quietly erase ancillary revenue, inflate support workload, and create risk with acquirers if dispute rates climb.

Below is a practical, operations-friendly breakdown of the root causes of visa chargebacks, plus a prevention checklist you can apply to embedded eVisa flows, white-label visa apps, or post-booking visa journeys.

What makes visa chargebacks different from “normal” travel disputes

A flight or hotel has obvious proof of consumption (boarding scans, check-in). A visa product often does not.

Common realities that raise dispute risk:

- Fulfillment is asynchronous: customers pay now, the decision may come later.

- Outcomes can be misunderstood: approval is never guaranteed, and entry is still at border officer discretion.

- Policies are nuanced: some fee portions are non-refundable, some are refundable only before submission.

- High stakes and short timelines: a traveler who realizes a problem 48 hours before departure is far more likely to dispute.

Also, consumer dispute rights are well established in the US. Under the Fair Credit Billing Act, cardholders can dispute certain billing errors and unsatisfactory transactions, which is why clarity, documentation, and responsiveness matter in your workflow (see the CFPB guidance on disputing credit card charges).

Visa chargeback root causes (what’s really driving disputes)

Chargebacks typically fall into a few buckets: fraud, processing errors, and “service” misunderstandings. In visa flows, those buckets map to specific, repeatable failure modes.

1) Confusing billing descriptors and “Who did I pay?” confusion

If a traveler sees a descriptor they do not recognize, they often default to “unauthorized.” This is especially common when:

- The visa service is white-labeled but the descriptor is not aligned to the traveler-facing brand.

- The descriptor is truncated (common on mobile banking apps).

- The traveler bought multiple travel items in one session and cannot match the charge.

Prevention idea: keep the payment confirmation page, receipt email, and descriptor language consistent. Make sure the receipt clearly ties the purchase to the itinerary (destination, traveler name, travel date).

2) “Service not received” because the traveler equates “submitted” with “approved”

Many customers assume payment equals instant issuance. When processing takes longer than expected, they dispute.

Typical triggers:

- The product page says “fast” but does not define realistic processing windows.

- Manual review occurs due to document quality or inconsistent data.

- The traveler never notices status emails, or they went to spam.

Prevention idea: set expectations twice, before purchase and after submission, and provide self-serve status access.

3) Refund policy friction, especially around non-refundable components

Visa fees often combine multiple components, such as government fees, third-party service fees, and optional expedite fees. If customers do not understand what is refundable and when, disputes rise.

Common friction points:

- No clear “refundability moment” (for example, refundable before submission, not after).

- No clear split of fee components at checkout.

- Cancellations handled via support only, which increases delays.

If you publish pricing content, align it with how disputes are handled, and use plain language. (SimpleVisa’s perspective on transparent fee composition is a helpful reference point: Fee for Visa: How Costs Are Calculated.)

4) Duplicate charges from retries, timeouts, or multi-tab behavior

Visa forms are often long, document uploads can fail, and travelers may refresh or retry. That can create:

- Duplicate authorizations that later capture.

- Two purchases by the same user across different devices.

- Confusion when a pending charge appears, then the final settled charge posts.

Prevention idea: implement idempotency for payment calls (where possible), show a “payment processing” interstitial, and email a receipt immediately.

5) Data-entry errors that lead to rework, delays, or refusal

If a traveler inputs a name that does not match the passport MRZ, uploads an invalid photo, or selects the wrong visa type, the downstream pain is predictable. Even when the underlying cause is user error, the payment dispute often lands on you.

Prevention idea: add validation and pre-submission review screens, especially for names, passport numbers, and dates. If you want a concrete example of how one data mismatch escalates operationally, see: Handling Name Mismatches on Tickets, Passports, and eVisas.

6) Fraud, account takeover, and “friendly fraud” in high-intent moments

Visa purchases are attractive to fraudsters because:

- A successful eVisa can be resold.

- Travelers buy close to departure, which compresses your time to detect risk.

- Chargebacks can be filed even after the service work was performed.

“Friendly fraud” (a real customer disputing a legitimate charge) can also happen when the traveler is stressed, missed a policy detail, or wants a faster refund than your process provides.

7) Border denial blamed on the visa purchase

Even with a valid authorization, a traveler can be denied entry for reasons outside the visa issuance itself. When the customer believes “your visa failed,” you can see disputes that are difficult to win if your communication is vague.

Prevention idea: clarify the product’s promise precisely: assistance with application and management, not an entry guarantee.

A quick root-cause matrix you can share with finance, support, and product

| Root cause | What the customer says | What’s usually happening | Best prevention lever |

|---|---|---|---|

| Descriptor confusion | “I don’t recognize this charge.” | Brand mismatch, truncated descriptor, no receipt found | Align descriptor to brand, instant receipt, itinerary-linked confirmation |

| Delays and uncertainty | “I never got my visa.” | Processing window not understood, manual review, missed comms | Clear SLAs, proactive status updates, self-serve tracking |

| Refund friction | “I canceled but wasn’t refunded.” | Policy unclear, refund window missed, slow support workflow | Upfront refund rules, fee split, fast cancellation path |

| Duplicate billing | “I was charged twice.” | Retries, multi-device, auth/capture confusion | Idempotency, duplicate detection, clear “pending vs posted” UX |

| Data errors | “Your service didn’t work.” | Incorrect passport/name, bad photo, wrong category | Field validation, document checks, review step |

| True fraud | “I didn’t authorize this.” | Stolen card, account takeover | 3DS, velocity checks, device/email verification |

| Friendly fraud | “This is not what I expected.” | Expectations gap, stress, urgency | Transparent promise, timestamps, strong evidence pack |

Prevention checklist (use this before you scale visa ancillary sales)

This checklist is designed to reduce both disputes and the operational triggers behind them. Treat it like a cross-functional launch gate.

Checkout and UX controls

- Show the processing timeline in plain language before payment, including what can cause delays (document quality, manual review, government checks).

- Disclose refundability rules at the decision point (before purchase), not buried in a footer.

- Break down fees clearly (for example, government fees vs service fees) if your commercial setup includes multiple components.

- Repeat the product promise in one sentence: what you will do, what you will not do (approval and entry are never guaranteed).

- Add a final review screen for passport name, passport number, nationality, and travel dates.

If you are optimizing conversion while lowering disputes, reducing form friction also helps. A good companion read is: Why Travelers Abandon Visa Forms and 6 UX Fixes That Convert.

Payments and fraud controls

- Use Strong Customer Authentication where applicable (for example, 3DS for card payments) and keep the authentication logs.

- Block obvious velocity patterns (multiple attempts across cards, rapid repeats, mismatched geolocation vs itinerary).

- Require email verification (at minimum) and store proof of verified contact.

- Detect duplicates by matching traveler name, passport number (hashed), destination, and travel date to recent purchases.

- Make “pending authorization” messaging explicit to reduce “I was charged twice” confusion.

Operational controls (the biggest chargeback reducer in practice)

- Send immediate receipts that include:

- What was purchased (destination, product type)

- Traveler name

- Next steps and timeline

- Support contact path

- Provide proactive status updates at meaningful milestones (received, in review, submitted, decision).

- Offer a fast path to fix common issues (photo rejected, missing document) without restarting the entire flow.

- Design a clear escalation route for urgent departures (for example, travel within 72 hours), with documented outcomes.

Support controls that prevent disputes before they start

- Surface self-serve answers inside the flow so customers do not need to email to understand status.

- Train agents on the top dispute triggers: refunds, timelines, descriptor, and what “submitted” means.

- Standardize refund communication: confirmation of request, expected timeframe, and what happens if the government fee is non-refundable.

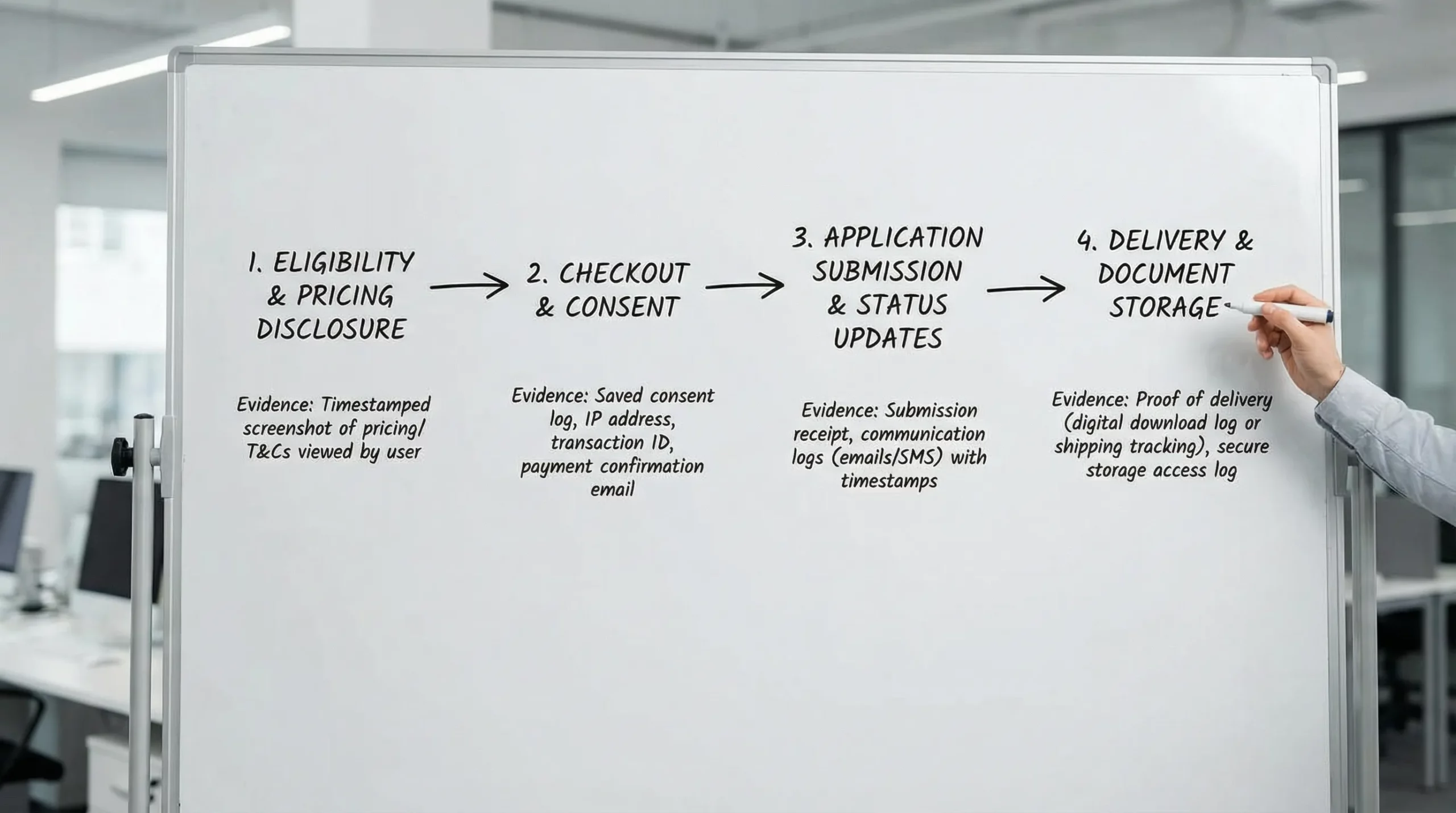

Evidence and recordkeeping (to win the disputes you cannot prevent)

You cannot eliminate all chargebacks. You can win more of them by building an evidence pack by default.

Keep:

- Checkout screens and logs showing policy acceptance (timestamp, IP, user agent).

- Payment confirmation, receipt delivery logs, and customer communications.

- Status timeline: when documents were received, when the application was submitted, and when updates were sent.

- Any user-provided data and files (securely stored), plus validation outcomes.

The “chargeback-proof” customer journey: what good looks like

When disputes are low, the customer journey usually has three qualities:

- Certainty (they always know what stage they are in)

- Control (they can fix issues and request help quickly)

- Clarity (they understand what they bought and what is refundable)

Where visa automation reduces chargebacks (without “fighting” customers)

Many teams try to solve chargebacks at the end of the process, by writing better representment responses. In visa workflows, the biggest wins usually come earlier: fewer errors, clearer expectations, and better status visibility.

A visa management approach that emphasizes guided applications and automation can reduce the upstream triggers that create disputes in the first place, especially:

- Fewer data mistakes through guided inputs and checks

- Clearer, more consistent traveler communication

- Better status visibility and handoffs

SimpleVisa’s platform is built for this kind of operational consistency, with options to integrate into booking flows via API, or launch via a white-label application and data services. If you are mapping this into your broader stack, you may also find it useful to reference: What Is Travel Document Automation? Definitions, Benefits, and Myths.

What to monitor weekly (so chargebacks do not sneak up on you)

Chargebacks lag behind the customer experience that caused them. Monitor leading indicators alongside the disputes themselves.

Recommended metrics:

- Dispute rate and dispute count (overall, and specifically on visa SKUs)

- Refund request rate and median time to refund completion

- Average time in each visa status (submitted, in review, decision)

- Support contacts per application (and top contact reasons)

- Application error rate (name mismatch, photo rejection, missing docs)

If you already track visa conversion and ancillary revenue, add disputes as a first-class KPI. SimpleVisa outlines KPI thinking here: 5 KPIs to Track After Deploying a Visa Management Platform.

A practical next step

If your visa attach rate is growing, treat chargeback prevention as part of product quality, not just payments operations. The highest ROI actions are usually the least glamorous ones: clearer policies, better milestone messaging, and fewer user-data errors.

If you want to reduce visa chargebacks while scaling ancillary revenue, SimpleVisa can help you operationalize a guided, trackable visa journey through an integration, a white-label app, or a custom data service. You can explore the integration paths at SimpleVisa and align the approach to your booking flow and support model.